Lines on the Map. Redlining and the Financial Architecture of America

Racial inequality in the United States is not accidental. It is designed. Redlining transformed racism into policy, embedding segregation into the financial and urban structure of American cities. Its consequences remain visible today.

There is a scene in Boyz n the Hood that should be shown at the start of every urban economics course. In it, Furious Style - the “wise man” of the movie, played by Lawrence Fishburne - gathers a group of kids from Compton and explains the real estate market in terms of a simple yet devastating mechanism of segregation. He talks about houses, prices, rates, “gentrification”, and invisible borders that determine who can live where. In other words, he explains that a neighbourhood is not just a place to live in. It is, first and foremost, a financial dispositif.

This scene is one of the most honest portrayals of American cities that Hollywood has ever produced. If you really want to understand why the United States is the way it is — expanses of suburbia and islands of downtown, roads that separate rather than connect — you have to start with houses. You have to consider the fact that living in America has been intimately connected with the country's financial infrastructure for decades.

As with many issues in contemporary US history, the roots of the problem can be traced back to the Great Depression. More specifically, to the plan implemented by Roosevelt in the mid-1930s to rescue the American economy, i.e. the New Deal. It was at this time that the importance of the real estate market in the credit cycle was recognised, and that housing was acknowledged as not only a private matter, but also a fundamental part of the asset structure of modern societies. As such, it requires standards, rules, and guarantees. Above all, it requires an entity — in this case, the state — to act as director and referee. This led to the creation of several institutions that would invisibly or visibly shape America in the decades to come, most notably the Home Owners' Loan Corporation (HOLC) and the Federal Housing Administration (FHA).

The contemporary real estate mortgage originated in 1930s America and was shaped by these two institutions, not on the basis of a romantic notion (the “dream of a house”), but of a bureaucratic and financial necessity: making credit manageable on a wide scale. Debt had to become a form of “economic citizenship”, not an exception or an aberration. For that to happen, a sustainable debt model had to be created, namely the real estate mortgage (equivalent to the Italian mutuo): longer duration, more affordable installments, “reduced” risk. It was the standardization of the future: an entire country learning to plan based on contracts.

However, the point is that every contract involves selection. If you are creating a “safe” market, you have to decide what is and what isn’t safe. The FHA and other federal agencies began to think in these terms: which areas are financeable, which neighborhoods guarantee that home values will grow at rates that offset interest rates and inflation, and which are at risk of “depreciation.” The language they use to express these considerations is cold and bureaucratic. But within that language, as is often the case in America, there is an implicit racial subtext which is not a bug in the system: it is one of its features.

For the risk, in this context, isn’t just an economic variable. It is a social judgment disguised as a technical criterion. For the FHA parameters, “risky” can mean “poor neighbourhood”, but also "unstable neighbourhood”. And, in many documents from that time, “unstable” meant one very specific thing: not white enough.

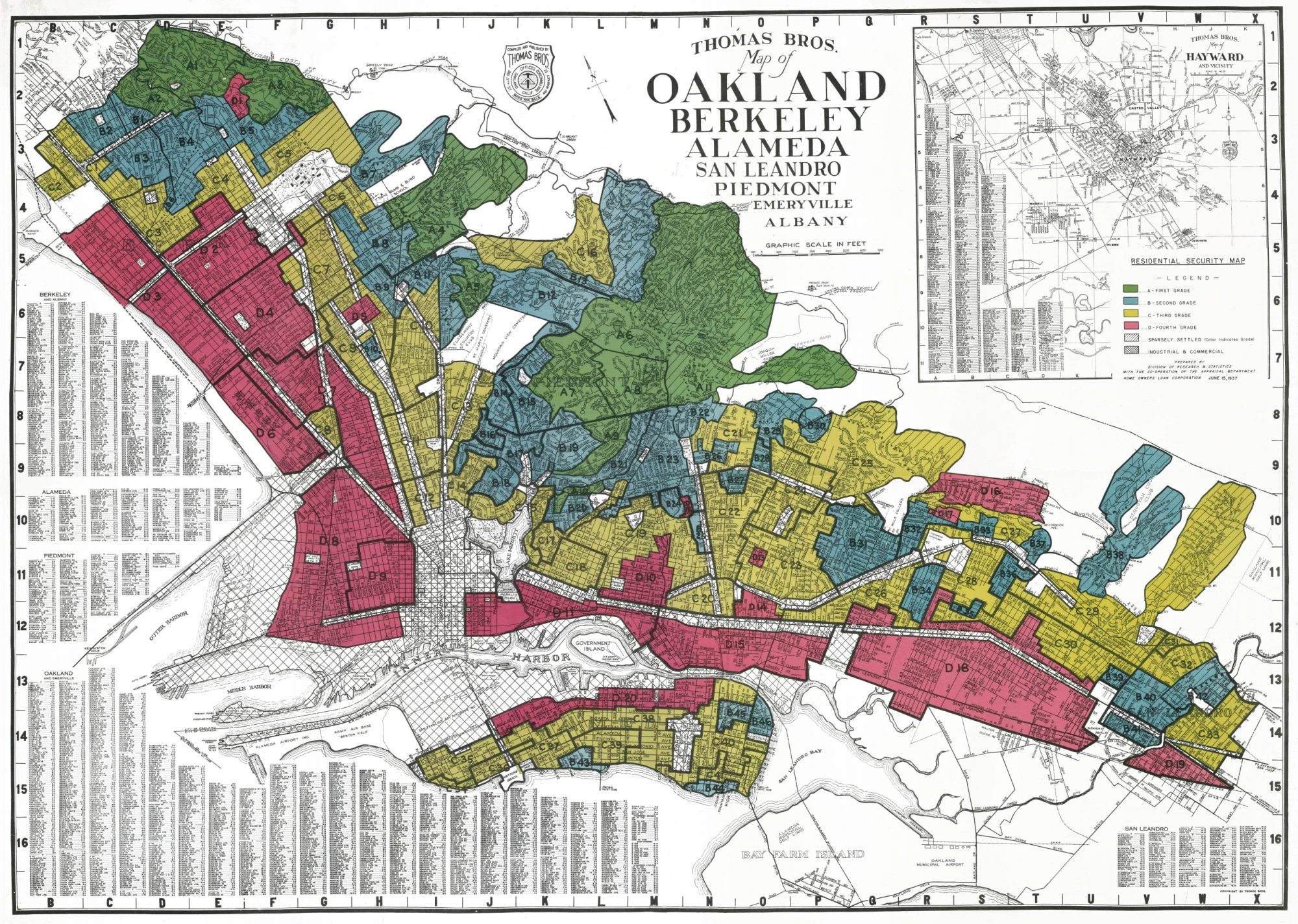

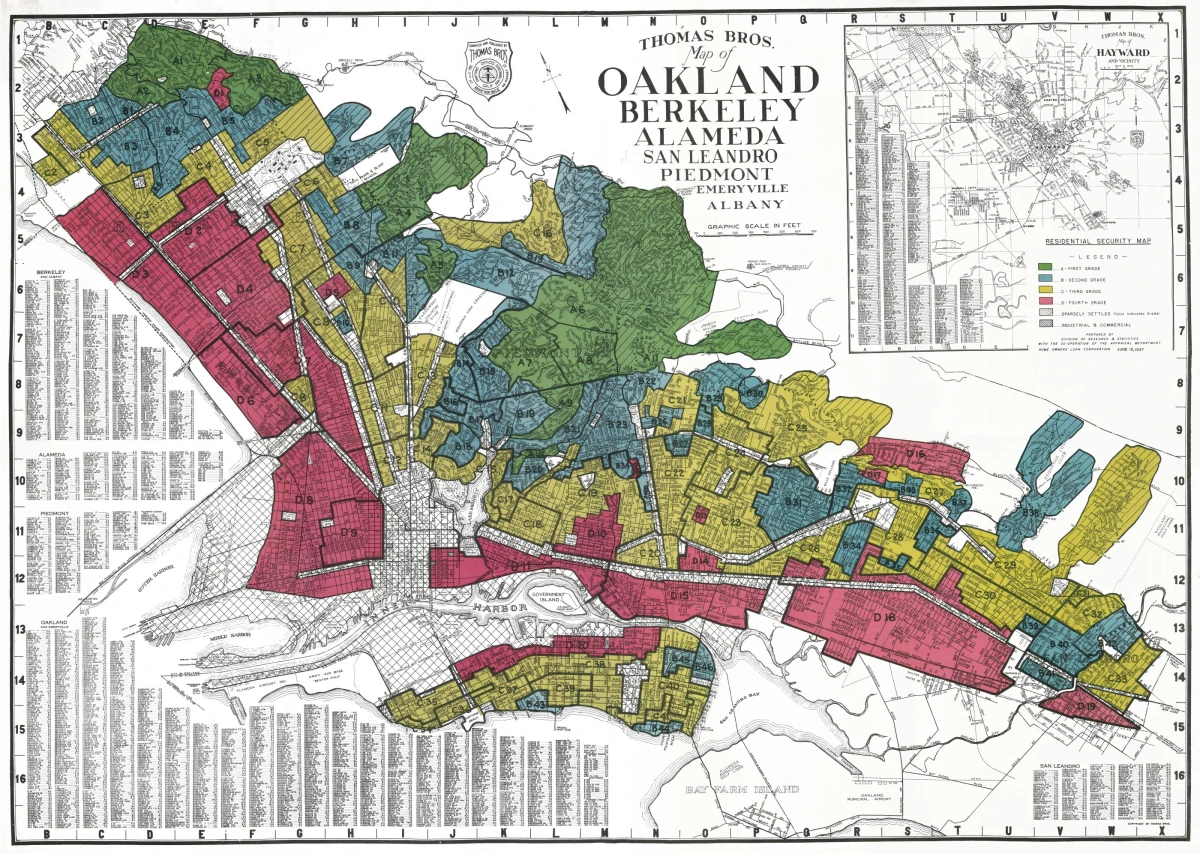

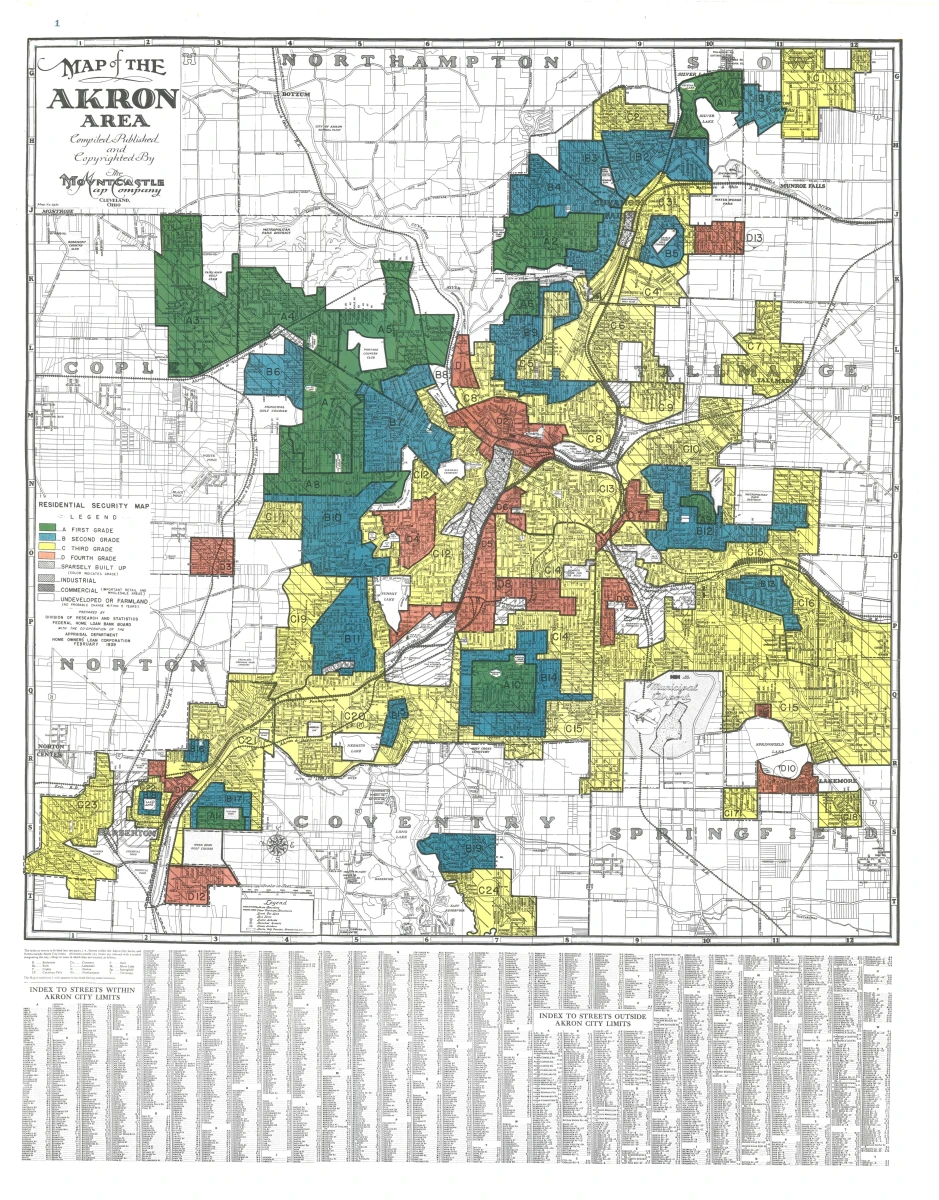

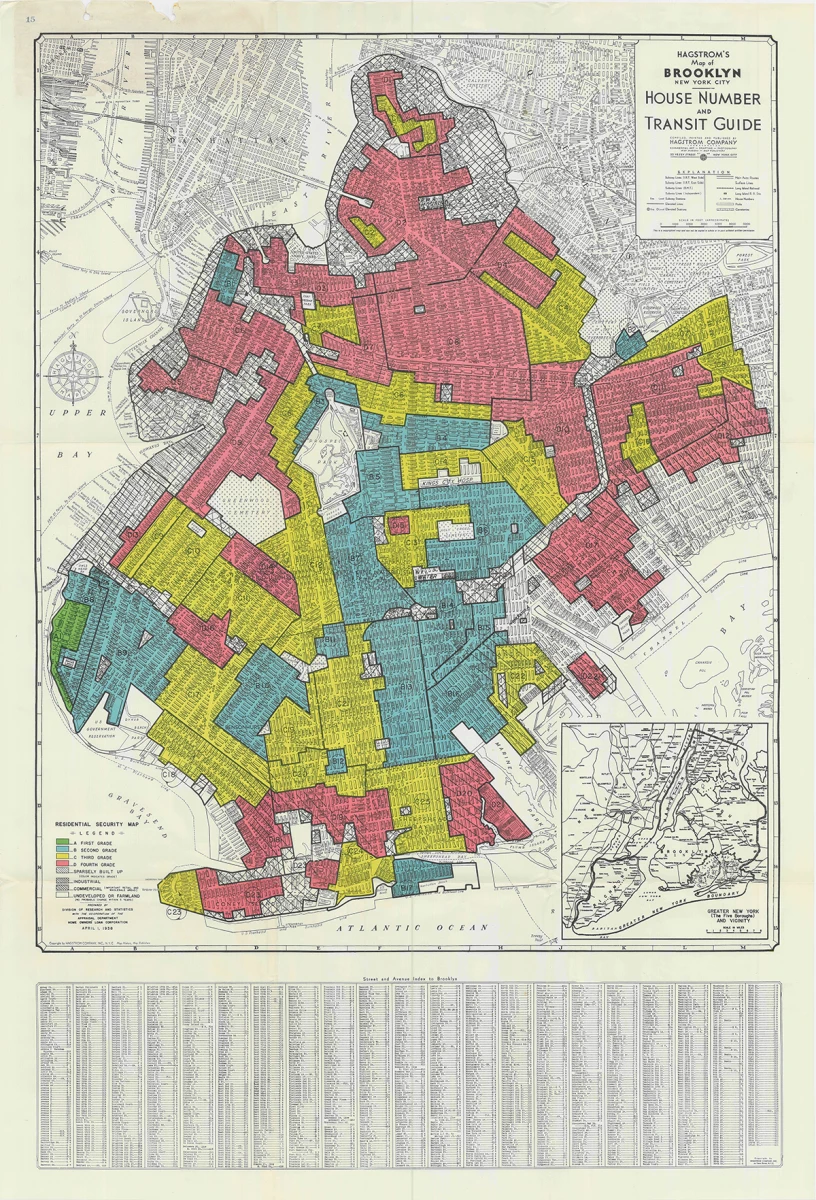

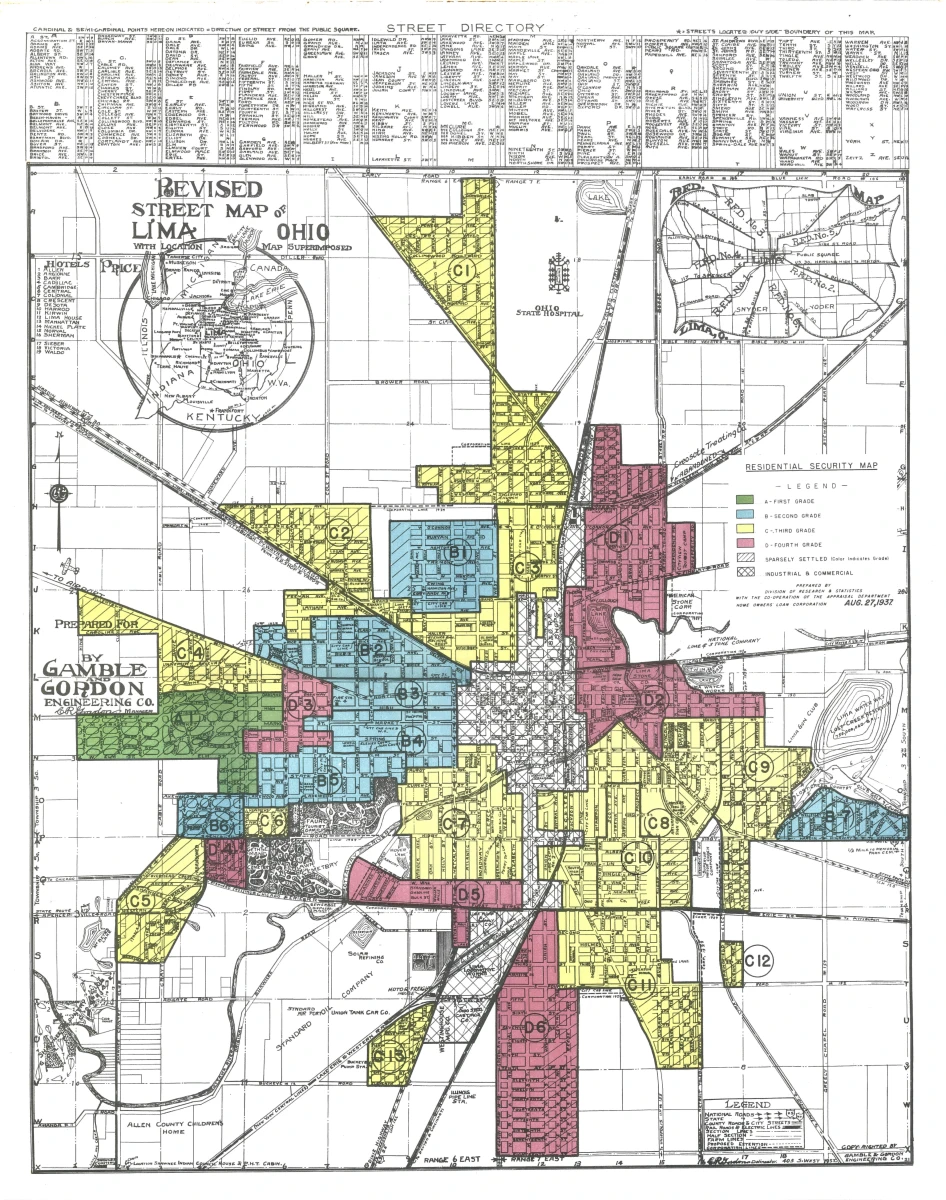

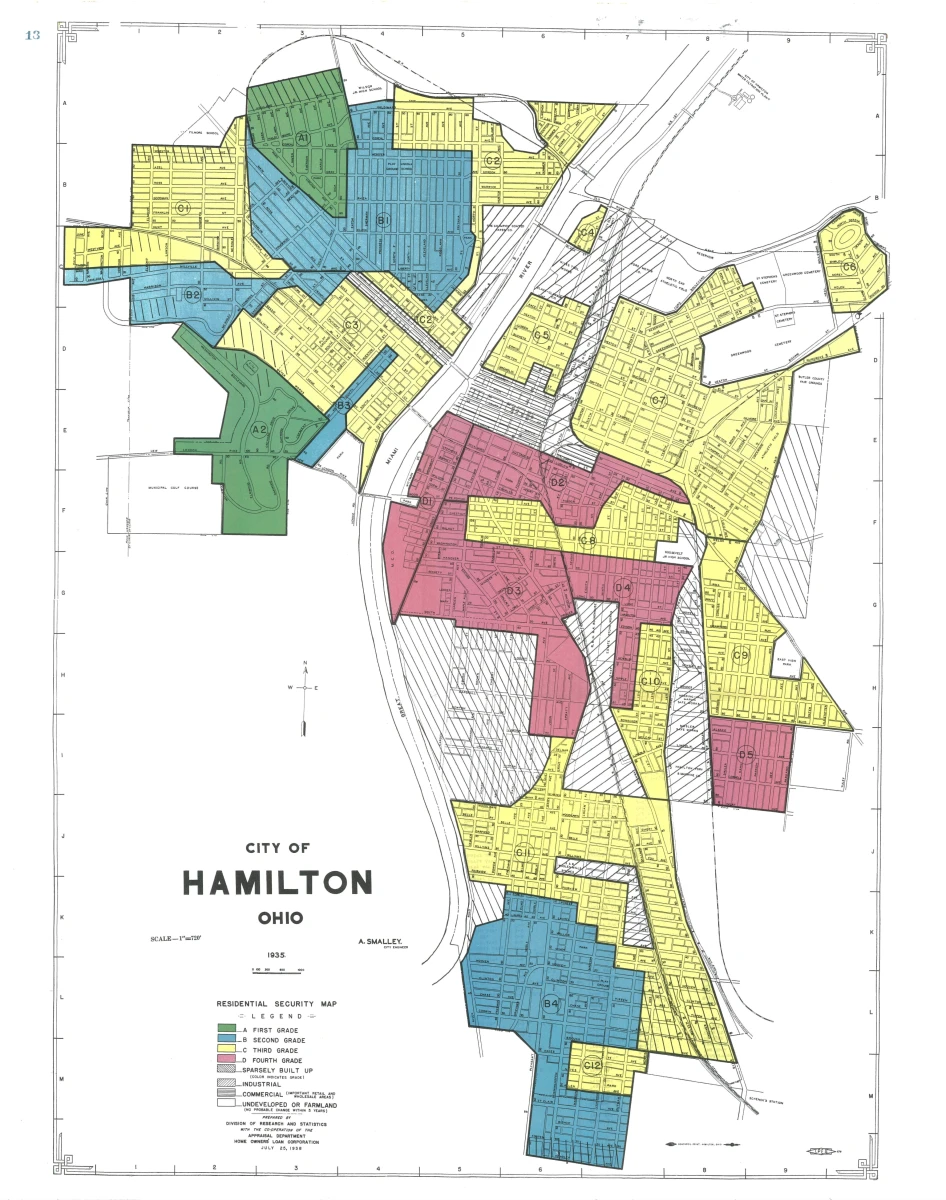

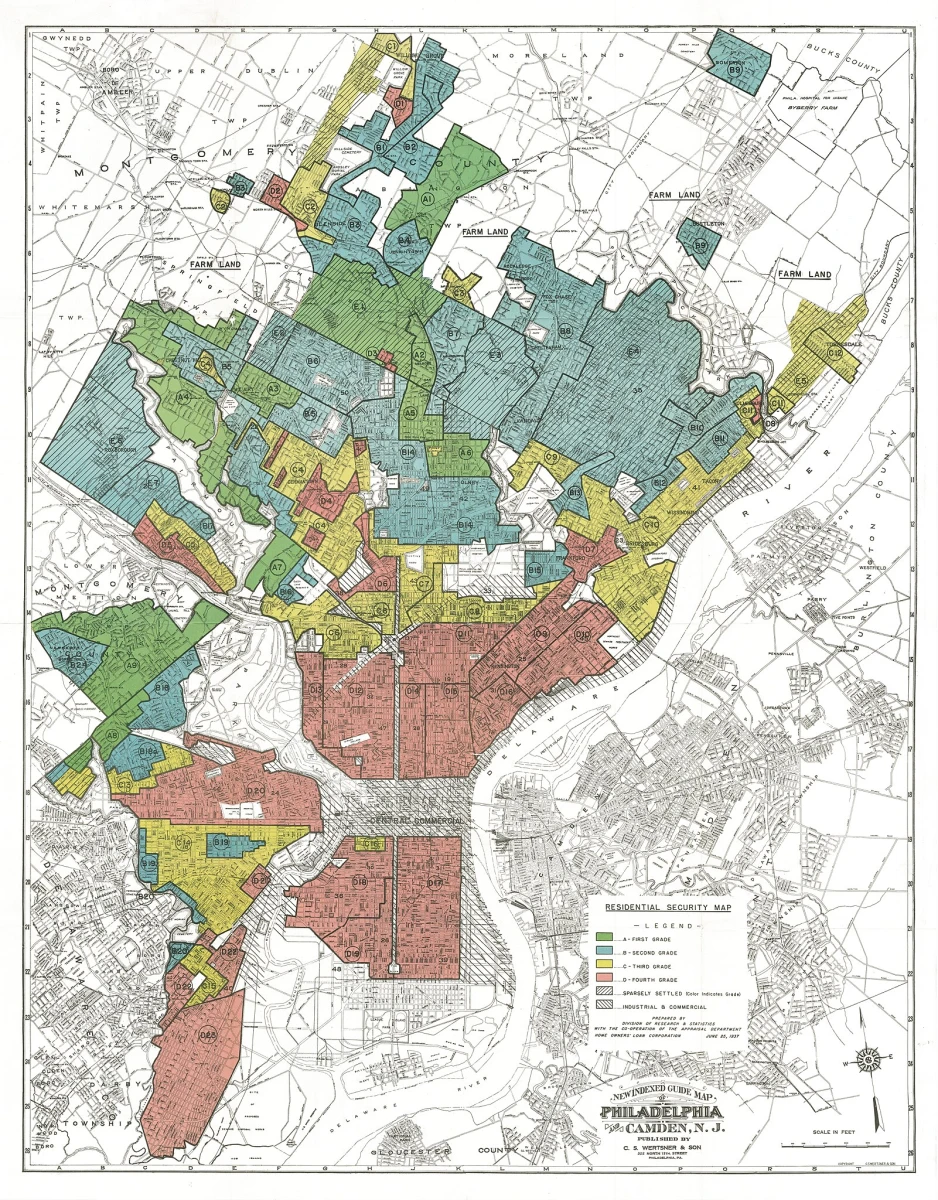

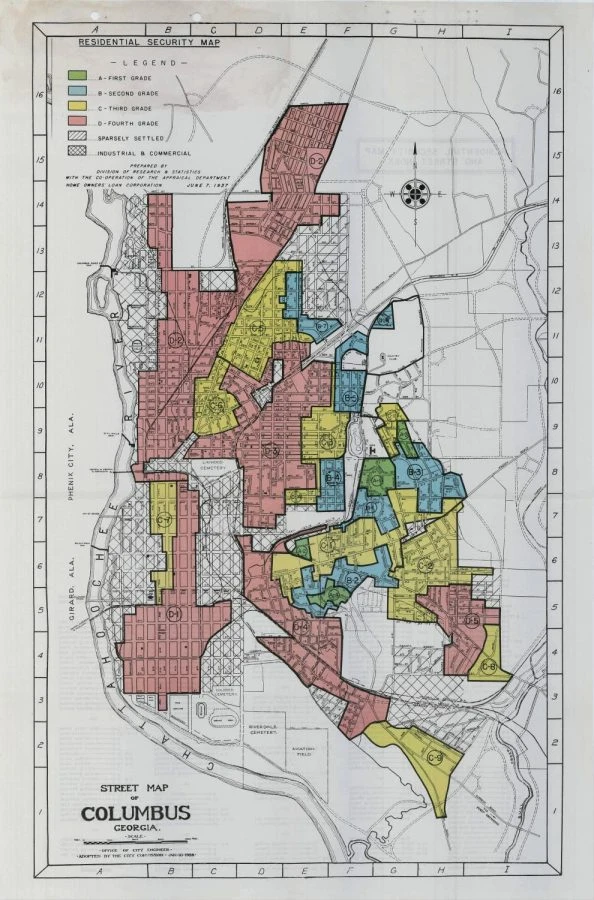

This is how we arrive at what would later be called redlining. In the 1930s, the HOLC began producing so-called Residential Security Maps: city maps in which neighbourhoods were classified according to their financial “reliability.” Green indicated the “best” areas, blue those that were still considered solid, yellow those “in decline”, and red those considered hazardous. Can you guess the racial composition of the hazardous areas?

From the outset, the modernization of American real estate has been accompanied by a Pynchionesque inherent vice: in order to govern the market, it must be made orderly; to do so, anything perceived as disorderly must be excluded. The house became the main tool through which the state built a middle class of property owners. At the same time, it became the filter through which it decides who can join that middle class and who cannot.

The next step - the truly decisive one - is how this “racial subtext” is transformed into economic grammar. Initially, racism entered the credit system as a cultural premise: a set of fears, stereotypes, and prejudices. But once these fears were incorporated into credit protocols, something more sophisticated and resistant happened: racism ceased to be merely a feeling and became a practice. A method. A shared rationality.

When federal agencies and banks started classifying neighbourhoods according to risk, the racial composition of an area became an environmental variable, like noise levels, like proximity to a factory, like traffic. This conversion produced a perverse effect, that is almost “ingenious” in its ability to survive over time: because, when discrimination relies on finance, it no longer needs to be defended as an ideology. It defends itself as an interest.

Previously, excluding Black people from white neighbourhoods required an explicit admission: “I don’t want you because I don’t like you”. Afterwards, however, it started to function as an economic logic: I’m not excluding you because “I don’t like you”, but because “you aren’t convenient for me”. This small linguistic twist changed everything, for it made segregation not just more acceptable, but also more contagious. The question is no longer whether you are racist. Instead, it becomes: do you want your house to lose value?

When the real estate market becomes the foundation of the American financial system, the home ceases to be merely a place and becomes the primary means of economic security for millions of people: their retirement plan, their savings, their insurance against uncertainty, and their collateral for obtaining other loans. If your home is your piggy bank, then anything that threatens its value becomes an enemy. Even if that enemy is, quite simply, a neighbour. You no longer need to be racist to behave like a racist. It is enough to be a homeowner.

This set in motion a chain of incentives that produced a new type of collective rationalisation. The average white citizen can tell themselves — and often literally does — that it is not discrimination, but “protecting their investment”. The short circuit, the loop, is as follows: prejudice at the origin gives rise to economic practice, which then returns to the source producing a new wave of prejudice. It is no longer “Blacks bring degradation”. It is: “The market thinks Blacks bring degradation, so I have to protect myself”. It is no longer “I don't want to live near them”. It is: “'I can't afford to live near them because this house is all I have”. Race is no longer an identity obsession. It is a property risk.

Segregation becomes a form of insurance. This transformation has a further, even more cynical effect: it makes racism a self-fullfilling prophecy through numbers. If a neighbourhood is perceived as “risky”, capital abandons it, or it strokes it with worse conditions. If capital abandons an area, it gets poorer. If it gets poorer, precarity, instability, and material issues increase. When material issues increase, property values fall. At this point, the neighbourhood becomes a ghetto, and the initial prophecy is realised. Not because it was true in the beginning. Because it was made true a posteriori. It is a self-fulfilling prophecy.

And when property values fall to their lowest point? What happens then? The same thing that Furious tells to the Compton kids. Someone comes along and buys land lots in the ghetto at bargain prices, promising to requalify them with money from long-term mortgages taken out by the same middle class that, by segregating minorities to protect its own assets, created the conditions for the ghetto to develop. The same middle class to whom, in the end, the neighborhood will be sold back once the requalification is complete, waiting for a ghetto to be created elsewhere. And the wheel starts turning again.